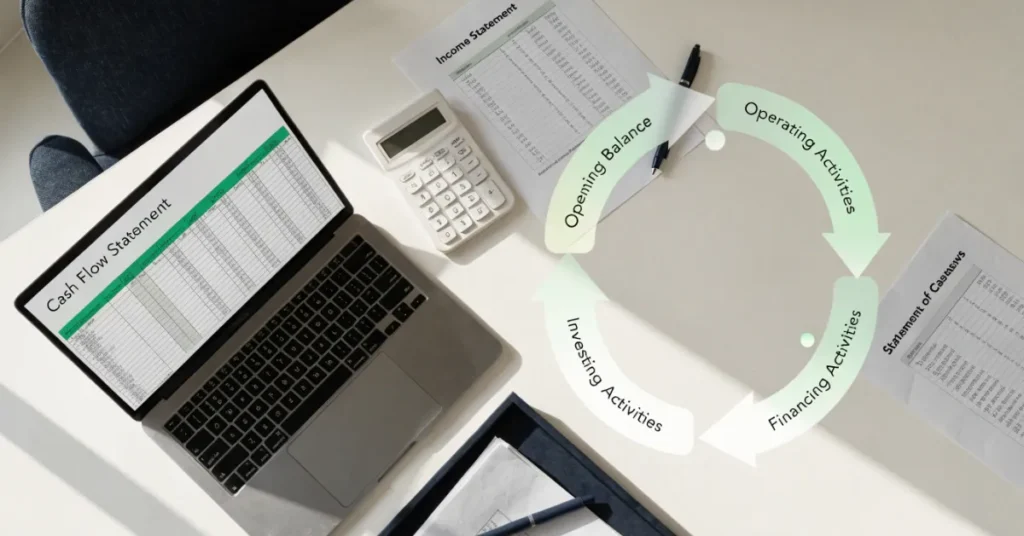

A Cash Flow Statement is one of the most important financial reports for any business. While a company may show strong profits on its income statement, it can still face financial difficulties if it does not have enough cash to cover everyday expenses. This is why understanding and preparing a cash flow statement is essential for business owners, accountants, investors, and financial managers.

What Is a Cash Flow Statement?

A Cash Flow Statement is a financial statement that reports the inflow and outflow of cash and cash equivalents during a specific accounting period. Unlike the income statement, which records revenue and expenses based on accrual accounting, the cash flow statement focuses only on actual cash transactions. Its main purpose is to show how effectively a business generates cash to fund operations, pay debts, invest in assets, and support future growth. It also helps identify whether a company has enough liquidity to meet its short-term financial obligations.

The cash flow statement is one of the three primary financial statements, alongside the balance sheet and income statement. Together, these reports provide a complete view of a company’s financial health and business performance.

Why Businesses Prepare a Cash Flow Statement

Businesses prepare a cash flow statement for several reasons:

- Monitor available cash for daily operations.

- Evaluate the company’s financial stability.

- Support budgeting and financial planning.

- Help lenders and investors assess financial performance.

- Improve decision-making for future investments.

- Identify periods of cash shortages before they become serious problems.

A well-prepared statement of cash flows also supports accurate financial reporting and helps management maintain healthy working capital.

Cash Flow vs. Profit

Many people assume profit and cash are the same, but they measure different aspects of a business.

| Profit | Cash Flow |

|---|---|

| Based on revenue minus expenses | Based on actual cash received and paid |

| Includes non-cash items like depreciation | Records only cash transactions |

| Shown in the income statement | Shown in the cash flow statement |

| May appear positive even without available cash | Reflects the company’s actual liquidity |

For example, imagine a business sells products worth $20,000 on credit. The sale increases profit immediately, but no cash enters the business until customers pay their invoices. As a result, the business may report healthy profits while struggling to pay suppliers or employee salaries.

This difference makes the cash flow statement an essential tool for evaluating real financial health rather than accounting profit alone.

Why Is a Cash Flow Statement Important?

A cash flow statement provides valuable insights that go beyond profitability. It helps businesses understand how cash moves through operations, investments, and financing activities, making it easier to maintain financial stability and plan for future growth.

Here are the key benefits of preparing a cash flow statement:

- Measures liquidity: Shows whether the business has enough cash to meet short-term obligations.

- Tracks cash inflows and outflows: Identifies where money comes from and where it is spent.

- Supports financial planning: Helps businesses prepare realistic budgets and forecasts.

- Improves cash management: Enables better control over daily business finances.

- Assists investment decisions: Helps management evaluate whether enough cash is available for expansion.

- Builds lender and investor confidence: Demonstrates responsible financial reporting and business performance.

- Identifies cash shortages early: Allows corrective action before liquidity problems affect operations.

- Strengthens working capital management: Supports healthier cash reserves and smoother business operations.

Regularly reviewing a cash flow statement allows businesses to make informed decisions based on actual cash availability rather than assumptions.

The Three Main Sections of a Cash Flow Statement

Every cash flow statement is divided into three major categories. Each section reports cash generated or spent on different business activities, giving stakeholders a complete picture of cash movement during the reporting period. Understanding these sections is the foundation for preparing an accurate statement of cash flows.

Operating Activities

Operating activities include the cash generated from a company’s primary business operations. These transactions occur during normal day-to-day business activities and are usually the largest source of cash flow.

Common operating activities include:

- Cash received from customers for goods or services.

- Payments made to suppliers.

- Employee salaries and wages.

- Utility bills and rent.

- Insurance payments.

- Income tax payments.

- Interest received or paid, depending on applicable accounting standards.

For example, if a retail store receives $80,000 from customers and pays $55,000 to suppliers, $10,000 in salaries, and $5,000 in operating expenses, the remaining operating cash flow reflects the net cash generated from daily business activities.

A consistently positive operating cash flow generally indicates that the business generates enough cash to sustain its operations without relying heavily on external financing.

Investing Activities

Investing activities represent cash transactions related to the purchase or sale of long-term assets and investments. These activities often support future business growth rather than daily operations.

Common examples include:

- Purchasing equipment or machinery.

- Buying office buildings or land.

- Selling fixed assets.

- Purchasing investment securities.

- Selling investments.

- Acquiring another business.

For example:

- A company purchases new manufacturing equipment for $40,000.

- It later sells an unused delivery vehicle for $12,000.

The equipment purchase appears as a cash outflow, while the vehicle sale appears as a cash inflow under investing activities.

Negative investing cash flow is not always a concern. Many growing businesses spend significant amounts on new assets to improve future productivity and profitability.

Financing Activities

Financing activities include cash transactions involving business owners, investors, and lenders. These activities affect the company’s capital structure and funding sources.

Examples include:

- Receiving bank loans.

- Repaying loan principal.

- Issuing company shares.

- Receiving investments from owners.

- Paying dividends to shareholders.

- Buying back company shares.

For example:

- A business receives a $100,000 bank loan to expand operations.

- It repays $15,000 of an existing loan.

- It distributes $8,000 in dividends to shareholders.

The loan received is recorded as a cash inflow, while loan repayments and dividend payments are recorded as cash outflows. Reviewing financing activities helps businesses understand how much they rely on debt or equity financing and whether their funding strategy is sustainable.

By analyzing operating, investing, and financing activities together, businesses gain a comprehensive view of their cash position. This information supports better financial planning, improves cash flow analysis, and helps management make informed decisions that contribute to long-term financial stability.

Information You Need Before Preparing a Cash Flow Statement

Before you prepare a cash flow statement, gather all the financial records that reflect your business’s cash transactions during the reporting period. Having complete and accurate information helps you classify cash movements correctly and reduces the risk of errors.

The following documents are essential:

- Income Statement: Provides details of revenue, expenses, and net profit for the period.

- Balance Sheet: Shows changes in assets, liabilities, and equity between two accounting periods.

- Bank Statements: Verify all cash received and payments made.

- Cash Receipts: Record money collected from customers and other sources.

- Payment Records: Include payments to suppliers, employees, lenders, and service providers.

- Previous Cash Flow Statement: Helps compare trends and reconcile opening cash balances.

- Loan Documents: Record new borrowings, repayments, and interest payments.

- Asset Purchase and Sale Records: Identify investing activities such as buying or selling equipment, vehicles, or property.

Keeping organized accounting records and up-to-date bookkeeping makes preparing a cash flow statement much faster and more accurate.

Step-by-Step Process to Prepare a Cash Flow Statement

Preparing a Cash Flow Statement becomes straightforward when you follow a structured process. Each step builds on the previous one, ensuring that every cash transaction is recorded under the correct category.

Step 1 – Calculate the Opening Cash Balance

Start with the amount of cash and cash equivalents your business had at the beginning of the accounting period. This figure usually comes from the previous period’s closing cash balance or the current balance sheet.

Cash equivalents include highly liquid investments that can quickly be converted into cash, such as short-term deposits or treasury bills.

Example

- Opening cash balance: $20,000

This amount serves as the starting point for calculating the cash movement throughout the reporting period.

Step 2 – Calculate Cash Flow from Operating Activities

Operating activities represent the cash generated or used in the business’s everyday operations. This section shows whether the company can generate enough cash from its core activities to sustain operations. Begin by identifying all cash received from customers. Then subtract all operating cash payments, including supplier payments, salaries, rent, utilities, insurance, and taxes.

Example

Cash received from customers:

- Customer payments: $120,000

Cash paid:

- Suppliers: $65,000

- Employee salaries: $22,000

- Rent and utilities: $8,000

- Income taxes: $5,000

Operating Cash Flow

$120,000 − ($65,000 + $22,000 + $8,000 + $5,000)

Net Operating Cash Flow = $20,000

A positive operating cash flow indicates that the business generates sufficient cash from its regular operations.

Step 3 – Add Investing Activities

Next, calculate cash generated from or spent on long-term investments and business assets.

Record all purchases of equipment, vehicles, machinery, buildings, and investments as cash outflows. Record proceeds from selling these assets as cash inflows.

Example

Cash Outflows:

- Purchased office equipment: $18,000

Cash Inflows:

- Sold old machinery: $6,000

Net Investing Cash Flow

$6,000 − $18,000

Net Investing Cash Flow = -$12,000

Negative investing cash flow often reflects business expansion and investment in future growth rather than financial weakness.

Step 4 – Add Financing Activities

Financing activities include transactions that affect the company’s funding, such as loans, owner investments, and dividend payments.

Include:

- New bank loans

- Owner capital contributions

- Share issuances

- Loan repayments

- Dividend payments

Example

Cash Inflows:

- Bank loan received: $40,000

Cash Outflows:

- Loan repayment: $12,000

- Dividends paid: $5,000

Net Financing Cash Flow

$40,000 − ($12,000 + $5,000)

Net Financing Cash Flow = $23,000

This section helps users understand how the business finances its operations and future growth.

Step 5 – Calculate Net Increase or Decrease in Cash

Once you’ve calculated cash flows from operating, investing, and financing activities, combine them to determine the overall cash movement during the accounting period.

Formula

Net Cash Flow = Operating Activities + Investing Activities + Financing Activities

Using the previous examples:

- Operating Activities: +$20,000

- Investing Activities: −$12,000

- Financing Activities: +$23,000

Net Cash Flow = $31,000

A positive result means the business increased its cash balance during the reporting period. A negative result indicates that more cash left the business than entered it.

Step 6 – Determine the Closing Cash Balance

Finally, calculate the closing cash balance by adding the net cash flow to the opening cash balance.

Formula

Closing Cash Balance = Opening Cash Balance + Net Cash Flow

Example

Opening Cash Balance: $20,000

Net Cash Flow: +$31,000

Closing Cash Balance = $51,000

This closing balance should match the cash and cash equivalents reported on the balance sheet. If the figures do not reconcile, review your accounting records for missing or incorrectly classified transactions.

Following these six steps ensures your cash flow statement is complete, accurate, and aligned with standard financial reporting practices.

Cash Flow Statement Format – Example

The format of a cash flow statement is designed to present cash movements clearly under the three main categories. While businesses may use different layouts depending on accounting software or reporting standards, the structure remains largely the same.

Below is a simplified example.

| Section | Amount |

|---|---|

| Operating Activities | |

| Cash received from customers | $120,000 |

| Cash paid to suppliers | ($65,000) |

| Salaries and wages | ($22,000) |

| Operating expenses | ($8,000) |

| Taxes paid | ($5,000) |

| Net Cash from Operating Activities | $20,000 |

| Investing Activities | |

| Purchase of equipment | ($18,000) |

| Sale of machinery | $6,000 |

| Net Cash from Investing Activities | ($12,000) |

| Financing Activities | |

| Bank loan received | $40,000 |

| Loan repayment | ($12,000) |

| Dividends paid | ($5,000) |

| Net Cash from Financing Activities | $23,000 |

| Net Cash Flow | $31,000 |

| Opening Cash Balance | $20,000 |

| Closing Cash Balance | $51,000 |

This format provides a clear summary of where cash came from, how it was used, and the amount remaining at the end of the reporting period. Most accounting software generates this report automatically, but understanding the structure helps you review and interpret the figures with confidence.

Direct Method vs. Indirect Method

Businesses can prepare a Cash Flow Statement using either the direct method or the indirect method. Both methods arrive at the same final cash balance, but they differ in how operating cash flow is calculated.

| Feature | Direct Method | Indirect Method |

|---|---|---|

| Starting point | Actual cash received and paid | Net profit from the income statement |

| Operating cash flow | Lists cash collections and payments | Adjusts net profit for non-cash items and working capital changes |

| Preparation | More detailed | Easier and faster |

| Data required | Cash transaction records | Financial statements |

| Business use | Less common | Most widely used |

| Main advantage | Clear view of cash receipts and payments | Simpler preparation and reconciliation |

| Main disadvantage | Requires detailed cash records | Less visibility into specific cash transactions |

Which Method Should You Use?

The direct method is useful for businesses that want a detailed view of actual cash receipts and cash payments. It offers greater transparency and helps management understand daily cash movements. The indirect method starts with net profit and adjusts for items such as depreciation, changes in inventory, accounts receivable, and accounts payable. Because it is easier to prepare using existing financial statements, it is the method most businesses use.

Regardless of the method you choose, the final cash flow statement should accurately reflect the company’s cash inflows, cash outflows, and closing cash balance. Understanding both approaches allows business owners, accountants, and financial managers to prepare reliable reports and make better financial decisions.

Practical Example of a Cash Flow Statement

Let’s look at a simple example to understand how a Cash Flow Statement works in a real business scenario. Imagine a small retail business preparing its monthly cash flow statement.

Business Transactions

- Cash received from customers: $150,000

- Payments to suppliers: $80,000

- Employee salaries: $25,000

- Rent and utilities: $10,000

- Purchase of new equipment: $20,000

- Sale of old equipment: $8,000

- Bank loan received: $30,000

- Loan repayment: $12,000

- Dividends paid: $5,000

- Opening cash balance: $35,000

Step 1: Calculate Operating Cash Flow

Cash Inflows

- Customer receipts: $150,000

Cash Outflows

- Supplier payments: ($80,000)

- Employee salaries: ($25,000)

- Rent and utilities: ($10,000)

Net Cash from Operating Activities

$35,000

Step 2: Calculate Investing Cash Flow

- Purchase of equipment: ($20,000)

- Sale of old equipment: $8,000

Net Cash from Investing Activities

($12,000)

Step 3: Calculate Financing Cash Flow

- Bank loan received: $30,000

- Loan repayment: ($12,000)

- Dividends paid: ($5,000)

Net Cash from Financing Activities

$13,000

Step 4: Calculate Net Cash Flow

Operating Activities: +$35,000

Investing Activities: −$12,000

Financing Activities: +$13,000

Net Cash Flow = $36,000

Step 5: Determine Closing Cash Balance

Opening Cash Balance: $35,000

Net Cash Flow: +$36,000

Closing Cash Balance = $71,000

This example shows that although the business invested in new equipment and repaid part of its loan, it still increased its overall cash balance because its operating activities generated strong positive cash flow.

Common Mistakes to Avoid When Preparing a Cash Flow Statement

Even experienced professionals can make mistakes when preparing a cash flow statement. Avoiding these common errors improves the accuracy of your financial reporting and helps you make better business decisions.

- Confusing profit with cash flow: Profit includes non-cash transactions, while a cash flow statement records only actual cash movements.

- Incorrectly classifying transactions: Record operating, investing, and financing activities in their appropriate sections.

- Ignoring the opening cash balance: An incorrect starting balance affects every calculation that follows.

- Missing loan repayments: Loan principal repayments belong under financing activities and should not be overlooked.

- Double-counting cash transactions: Ensure each cash movement appears only once.

- Failing to reconcile balances: The closing cash balance should always match the cash reported on the balance sheet.

- Using incomplete financial records: Missing invoices, receipts, or bank transactions can produce inaccurate reports.

- Overlooking non-routine transactions: Asset sales, insurance claims, or one-time payments should also be included where appropriate.

Reviewing your records carefully before finalizing the statement helps reduce errors and improves financial accuracy.

Best Practices for Accurate Cash Flow Statements

Preparing a reliable cash flow statement requires more than simply entering numbers. Following proven accounting practices improves consistency and supports stronger financial management.

Consider these best practices:

- Update bookkeeping records regularly.

- Reconcile bank accounts every month.

- Separate personal and business expenses.

- Monitor cash flow trends instead of reviewing reports only at year-end.

- Keep invoices, receipts, and payment records organized.

- Verify calculations before publishing financial reports.

- Use accounting software to automate calculations and reduce manual errors.

- Compare current cash flow with previous reporting periods.

- Review working capital regularly.

- Prepare cash flow statements consistently, whether monthly, quarterly, or annually.

These habits make it easier to identify financial issues early and improve long-term cash management.

Tools That Make Cash Flow Statement Preparation Easier

Modern accounting tools simplify the process of preparing a cash flow statement by automating calculations, organizing financial records, and generating reports in minutes.

Some of the most useful tools include:

- Accounting software: Automatically records transactions and generates cash flow statements.

- Spreadsheet templates: Suitable for freelancers, startups, and small businesses with simple financial records.

- Cloud bookkeeping platforms: Allow real-time collaboration between business owners and accountants.

- Enterprise Resource Planning (ERP) systems: Integrate accounting, inventory, payroll, and financial reporting into a single platform.

- Financial dashboards: Provide visual insights into cash inflows, cash outflows, liquidity, and business performance.

Choosing the right tool depends on your business size, transaction volume, reporting requirements, and budget. Regardless of the solution you use, accurate bookkeeping remains the foundation of reliable financial reporting.

Simplify Your Financial Reporting with Ripple Business Setup

Preparing a Cash Flow Statement accurately requires organized financial records, proper bookkeeping, and a clear understanding of accounting principles. If you need expert assistance, Ripple Business Setup can help with bookkeeping, financial reporting, accounting, VAT, corporate tax, and business advisory services. Contact Ripple Business Setup at +971 50 593 8101, email info@ripplellc.ae, or WhatsApp +971 4 250 0833 to discuss your business requirements and receive professional support tailored to your financial reporting needs.

FAQ

What is the purpose of a cash flow statement?

A cash flow statement shows how cash moves into and out of a business during a specific period. It helps business owners evaluate liquidity, manage cash effectively, and ensure there is enough money to meet financial obligations.

What are the three sections of a cash flow statement?

The three main sections are:

- Operating activities

- Investing activities

- Financing activities

Together, these categories explain all major cash movements within a business.

What is the difference between cash flow and profit?

Profit measures revenue minus expenses, including non-cash items such as depreciation. Cash flow measures the actual cash received and paid during the reporting period. A profitable business can still experience cash shortages if customers delay payments or expenses exceed available cash.

Which method is better: direct or indirect?

Both methods produce the same ending cash balance. The direct method provides greater visibility into actual cash receipts and payments, while the indirect method is easier to prepare and is more commonly used in financial reporting.

How often should a business prepare a cash flow statement?

Most businesses prepare a cash flow statement every month. However, quarterly and annual statements are also common for financial reporting and compliance purposes. Regular reporting helps businesses identify trends and respond quickly to cash flow challenges.

Can a profitable business have negative cash flow?

Yes. A business may report strong profits while experiencing negative cash flow if it has high accounts receivable, significant inventory purchases, or large capital expenditures. This is why monitoring cash flow is just as important as tracking profitability.

Is a cash flow statement required for small businesses?

While requirements vary depending on accounting standards and reporting obligations, preparing a cash flow statement is highly recommended for businesses of all sizes. It improves financial planning, supports better decision-making, and helps business owners maintain healthy cash reserves.

Final Thoughts

A Cash Flow Statement is more than a financial report it is a practical tool for understanding how money moves through your business. By tracking cash inflows and cash outflows, you gain valuable insights into liquidity, operating performance, investment activities, and financing decisions. Preparing a cash flow statement begins with accurate bookkeeping, organized financial records, and a clear understanding of operating, investing, and financing activities. Following a structured process helps ensure your statement reflects your business’s actual cash position and supports better financial planning.

Disclaimer: This article is intended for general informational and educational purposes only and should not be considered accounting, tax, financial, or legal advice. Every business has unique financial circumstances. Consult a qualified accounting or financial professional before making business or financial decisions based on the information provided.